DJC#011 – Dependent Dollars: A Guide To Flexible Spending Accounts

When it comes to taking care of our families, we want to ensure they’re taken care of while being mindful of our finances. That’s where Dependent Care Flexible Spending Accounts (DCFSAs) come into play – not to get mixed up with the the other type of FSA is a Health Care Flexible Spending Account. FSAs, as I will refer to them going forward, offer some cool financial perks, helping us save money on our dependents’ healthcare expenses.

Today I’m going break down FSAs in Dad talk, explore their benefits, and show you how they can be a game-changer for managing your family’s healthcare finances. Let’s go!

What the ____ is an FSA?!

A Flexible Spending Account (FSA) for dependents is an employer-sponsored thing that lets you stash away some of your hard-earned cash before taxes to cover eligible dependent care expenses for your family.

Think about those costs that you are already incurring on a regular basis – child care, before/after-school care, camps, etc. This is a way to get a tax break on that same money. You’re already spending it, so why not get the tax advantage too? The beauty of it all is that by using an FSA, you save money while providing essential care for your little ones. Win-win!

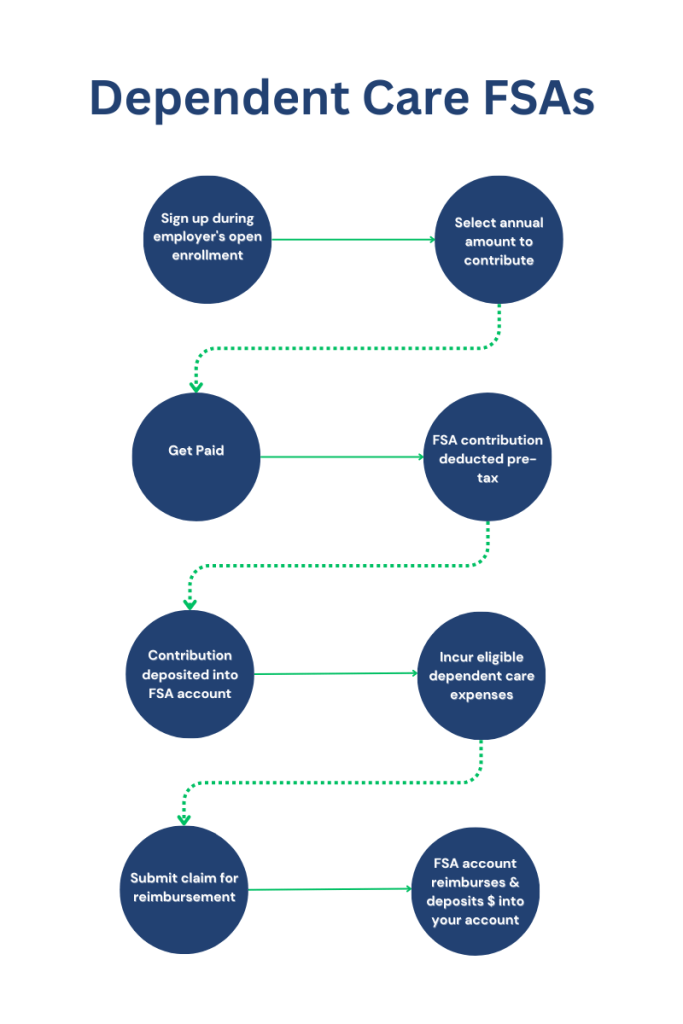

When you’re setting up your benefits through your employer, you can elect to sign up for and FSA and select the the total annual contribution to your FSA account. Typically this is done during your company’s open enrollment, but the IRS understands life doesn’t alway line up within that time frame (your child likely won’t be born during your open enrollment!) so there are some “life events” that are the exceptions –

- Marital status changes

- Number of dependents change

- Employment status of employee and/or spouse changes

- Residence changes

- Dependent care cost changes

FSA Limits

In 2023, the maximum contribution is $5,000 for singles or couples filing jointly, or $2,500 per person if married filing separately on your taxes. There is a minimum contribution of $100 required as well. Limits could potentially change each year, so remember to look before choosing your contribution amount.

Based on the amount you elect, your employer will break that down evenly across the number of paychecks you receive annually. If you get paid weekly, you’ll have a smaller amount pulled out from your checks, and if you get paid monthly, it’ll be a larger amount. In the end, it will average out your annual contribution amount over those pay periods.

Where Does My FSA Money Actually Go?

Great question! When you get your paycheck, you will see the amount subtracted before your federal, state and social security taxes are applied. Don’t worry, the money is not gone, it’s just been relocated to your FSA account.

Your employer will contract with a company to manage this process, but you are responsible for managing your account. Each paycheck you will see the money taken out of your paycheck and deposited into you FSA account. From there, you can start using it to pay for qualified dependent care expenses.

Who’s Eligible for An FSA?

For dependent care FSAs, eligibility is based primarily on someone who cannot take care of themselves. By rule, your dependents must considered qualified by definition. What is a qualified dependent? They are:

- Your dependents who are under 13 years old

- Your dependents who are physically/mentally incapable of caring for themselves, and live with you at least 6 months of the year

- Your spouse who’s physically/mentally incapable of caring for themselves and live with you at least 6 months of the year

There are other specifics around the definition of a dependent regarding that person’s gross income and tax filing status (I’m not diving into that here, so it’s recommended to consult with a tax advisor regarding those Qs).

What’s Eligible for An FSA?

So this list may not be like that resort you stayed at in Playa del Carmen – all inclusive – but it will give you a general idea what you can claim and use your newly funded FSA account towards:

- Child care

- Preschool

- Before or after school care

- Summer day camp

- Au pair

- Babysitting (while you’re working or going to school)

- Nanny

There definitely could be others, so be sure to check you provider’s program rules. Generally education or even tutoring is not something that are eligible expenses…and unfortunately neither are those hip-hop dance classes.

Ok, So How Do I Use This FSA Thing?

There are two ways to go a bout using your FSA account – direct pay from your account, or reimbursement from your account for incurred expenses. I’ve done it both ways – typically the reimbursement method is going to be use more frequently I’ve found in my experience.

Since summer is here, or almost here depending on where you live, let’s use this as an example – Say you have your child signed up for and art summer camp that’s $100 for the week (I know, what a deal!). After you’ve paid for camp and you child learned new art skills to become the next Banksy, you log into your FSA account and upload your receipt. You’ll need to have your child’s name, camp’s name, date of service, type of service, amount of the expense and the camp’s Tax ID Number (TIN) – so if it’s not on the receipt, make sure ask for it!

From there you’ll submit your claim and wait for it to be reviewed. Once it’s approved, the money will be sent to your bank account that you linked to your FSA account when you signed up. In a couple of days you’ll have completed the cycle and you’ll have reimbursed yourself essentially and paid $0 in taxes on that money. If there’s any issues with your claim, you’ll be notified what the issue so you can resolve it – maybe you forgot to include that TIN!

Most FSAs do partial reimbursements too. Say for our example that you only had $50 in your FSA account. You could submit your claim with the $100 receipt, and your FSA account will reimburse you the $50 that in it. When your FSA account gets funded from your next paycheck and has $50 in it, then they’ll process the remaining $50 of your claim.

Is It True…If You Don’t Use It You Lose It?

One thousand percent, yes. If you do not use all of your FSA money within the allotted time frame set by your employer, you lose the money and it goes back into your employer’s account, which they’ll use to cover admin costs, keep the funds as part of the biz, or elect to return funds to employees in a uniform manner.

It is very important when you are making your elections to have a clear picture of what your dependent care costs are going to be for the year. The younger your child is, and more child care you need, the quicker you’ll hit your limit. When my son was young, we probably hit the annual limit by the middle of the year, if not sooner. But as he’s gotten older, the cost for child care have gone down…although summer camps can be pretty damn expensive! So instead of automatically maxing out each year, my wife and I have strategically estimated our costs for the year because we definitely want to make sure we use it and don’t lose it.

Pay attention to the time periods. And grace periods? They give you extra time after the plan year ends to use up any remaining funds from the previous year. It’s like having bonus lives in a video game—more chances to score savings!

FSA Tax Benefits

Some you might be reading and saying, sure I can do this but why should I bother? Seems like a lot of work. It’s a little bit of work, but in the end you’re trying to reduce your Adjusted Gross Income (AGI) to reduce your taxable income. Would you do a little work to save some money?

Did you know if you max out your FSA at $5,000 and you’re in the 24% tax bracket, you could save up to $1,200 a year! Check out the HealthEquity FSA learning page for more info and their FSA calculator as it has a lot of great resources. I was lucky enough to use their FSA with my previous employer, and it was super easy to use and get reimbursed quickly.

Call To FSAction

Like anything in life, it’s great to learn, but kind of pointless unless you apply it to your life. I challenge every single one of you to sign up (or continue to sign up) for an FSA and use it to benefit your bank account. I also ask that you pay it forward and share this knowledge with other parents in your lives to make sure they are taking advantage of FSAs.

*Update: I recently learned from experience something to add. I’m not sure if this is the same with all FSAs, but what I experienced was only being able to make a claim during the time when I was working at my previous employer. I changed jobs earlier this year and my FSA benefits expired on February 28, which means I could only make a claim for any money I directed to my FSA account from January 1 – February 28, and only if I actually incurred an eligible expense during the same period. Unfortunately I did not incur any, and when I went to try to claim a week of summer camp that I ironically paid for four days after my last day of benefits, I was told…sorry Charlie. Just wanted to pass that along. Always check the details of your benefit.

Leave a comment