DJC#020 – 529 Accounts 101: A Simple Guide to Educational Investing

This is the third installment of Start Investing in Your Child’s Future Finances Today trilogy. We’ve gone over high yield savings accounts for their short-term savings. We tackled UTMA/UGMA accounts for their long-term investing that you manage until they become an adult. Now we’re going to dive into 529 accounts to supercharge saving for your child’s future educational costs.

What is a 529 Account?

Alright, let’s break it down. A 529 account is a specialized savings plan designed to help you save money for your child’s future education expenses – whether it’s college, vocational school, or other qualified higher education programs. It’s like having a NOS for your child’s educational journey vehicle.

A couple of things to consider to open a 529 account: you must be a US resident, at least 18-years old, and have a Social Security or tax ID number. Buttttt…you don’t even have to be the parent to open one!

Benefits of 529 Accounts

Now, here are some reasons why 529 accounts are total game-changers:

- Tax Advantages Galore: The best part? Your contributions to a 529 account are made with after-tax dollars, which means your investment earnings grow tax-free! And when you withdraw the money for qualified education expenses, you won’t owe any federal taxes. That’s a win-win for your wallet!

- Flexibility, Baby: 529 accounts offer great flexibility. You can use the funds for a wide range of education-related expenses, such as tuition, books, supplies, and even room and board. It’s like an all-access pass to covering your child’s college dreams.

- No Income Limitations: Unlike some other education savings plans, 529 accounts have no income limitations. That means families of all income levels can take advantage of this fantastic savings tool.

- Control in Your Hands: As the account owner, you maintain control over the funds, so you can make adjustments as needed. You’re the driver of this financial racecar!

Tips to Supercharge Your 529 Account

- Start Early, Reap Big: The sooner you start saving, the more time your investments have to grow. Even small, regular contributions can make a big difference over time.

- Team Effort: Don’t forget to get the family involved! Grandparents, aunts, uncles, and friends can also contribute to your child’s 529 account, adding even more fuel to the savings fire.

- Dream Big, Save Big: Have big educational dreams for your child? You can save in multiple 529 accounts, giving you the freedom to target specific educational goals.

- Stay Informed: Keep an eye out for any updates or changes to 529 plan rules. Being informed will help you make the most of your account.

Starting A 529 Account

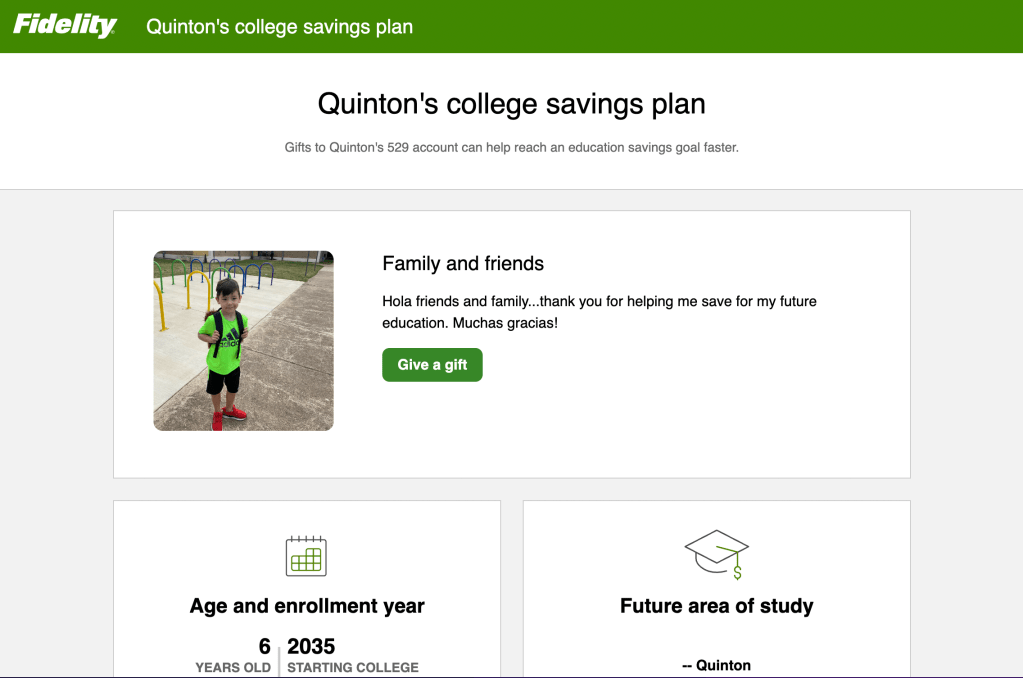

How do I get a 529 account, you ask? It’s simple. You can sign up at most major financial institutions. I’m a fan of Fidelity and Vanguard due to their low fees and solid funds. We went with Fidelity on this one – mainly because it was really easy to set up a shared page for your child’s account. You can edit the message on the page and share the link to friends and family. Birthday coming up? Send them the link. Christmas time? Send them the link.

Take a look at our son’s 529 page below. Feel free to donate while you’re checking it out!

Things to Consider

As mentioned, there is some flexibility with a 529. If you don’t use the money for college or other educational expenses here are some things to think about:

- Use It Or Don’t Lose It: You will not lose your money if it’s not used.

- Next Up: If you don’t use the money for your child’s education expenses, the money can still be used for post-secondary education on another child, niece, nephew or grandchild.

- Uncle Sam: If you withdraw the money for expenses unrelated to education you may owe taxes on the earnings withdrawn as well as a 10% penalty. The portion of the withdrawal that is made of of your contribution is not taxed (that’s the money you put in and was already taxed before you invested it). The earnings would be subject to the taxes and 10% penalty.

- Lower Education: Now you can now even use up to $10k per year on elementary, middle or high school.

5-2-9 Action

A 529 account is a great way to start saving and investing for your child’s educational future. With college costs so expensive these days, this is a great vehicle to use for your child. Just like in any other scenario, the sooner the better so that compound interest can kick in. Make sure to do your research to find out what’s best for your family’s situation.

One major consideration to add here before I go. College costs are high, and likely to continue to skyrocket. The thought of foregoing college is a reasonable one these days. I’m not sure if our son will end up going to college. In my day, the idea was just to get a degree and someone will hire you…but those days are over.

Is it worth it for you/your child to spend so much money on a degree and likely need to take out loans that won’t be paid off for years and years? I think it depends. Are they going to be a doctor, lawyer, scientist? Then most definitely. Are they going to be a writer, publicist, artist, business person? Hmmm, maybe not? There are a lot of question marks around the future of higher education. I do think the structure could change (it already is), but I do think there will still be a need to pay for learning skills…it just might not be at a university.

Leave a comment